IMPORTANT NOTE: As of November 11, 2022, the student loan forgiveness application has been suspended due to a challenge in federal court. We will update this article as more information becomes available.

Student loans can be a significant obstacle to achieving your financial goals. In fact, the average college graduate who used loans to fund their education graduates with $25,921 in debt. This equates to a payment of about $275 per month.

Fortunately, new legislation seeks to provide some relief for 43 million of the 45 million Americans with student loans. This loan forgiveness program could help reduce your long-term liabilities and monthly expenses. With lower debt and more money each month, you could make more progress toward achieving your retirement goals.

Who qualifies for student loan forgiveness?

The student loan forgiveness program applies to most types of existing federal loans. However, there are income stipulations that you should understand before applying.

Borrowers with Existing Federal Loans

You must have federal student loan debt acquired before June 30, 2022 to qualify for loan forgiveness. Any new loans issued after that date are not currently eligible for forgiveness.

Types of student loans eligible for forgiveness include:

- William D. Ford Federal Direct Loan Program loans

- Federal Family Education Loan [FEEL] Program loans

- Federal Perkins Loan Program loans that are held by the Department of Education

- Subsidized and unsubsidized Stafford loans

- Parent PLUS loans

- Graduate PLUS loans

If you have any of these types of loans, you could be eligible for forgiveness, even if you are in default. However, private education loans are not currently eligible for this program.

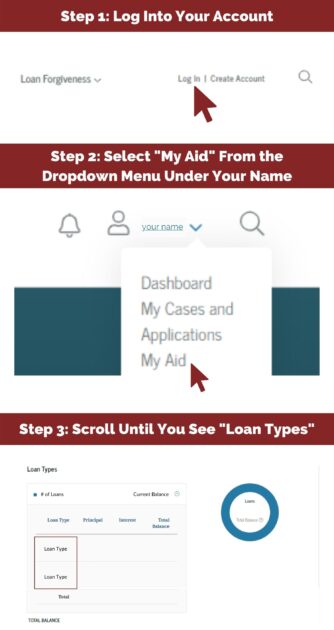

To determine which types of loans you have, log into studentaid.gov and navigate to the “My Aid” section in the dropdown menu under your name. There you will find a “Loan Breakdown” which details all federal loans you have received, including those you have already paid.

Borrowers with Income Under Certain Limits Are Eligible for Forgiveness

The student loan forgiveness program is subject to income limits. For individual filers and those that are married filing separately, you must have earned less than $125,000 in either 2020 or 2021. For those that are married filing jointly, head of household, or qualified widow(er)s the limit is increased to $250,000. The income limit is based on your Adjusted Gross Income [AGI], which you can find on line 11 of your 1040.

Dependent Students Are Eligible for Forgiveness

Dependent students are those who meet the following criteria:

- Born after January 1, 1998

- Enrolled in an undergraduate program between July 1, 2021, and June 30, 2022

- Unmarried

If you meet these criteria, you could qualify for the full amount of loan forgiveness, but your eligibility will depend on your parents’ income rather than your own.

If you are a dependent student, you should apply for forgiveness using your own information, not your parent’s. Once your application is processed, you may be contacted to provide additional information including your parents’ income.

Parents with Student Loans Are Eligible for Forgiveness

If you are a parent with federal student loans for your child’s education, you can apply for loan forgiveness. If this is the case, you should apply with your own information, not your child’s. Your application will be processed separately from one submitted by your child if they also have loans for their education.

How much will be forgiven?

The amount of your student loans eligible for forgiveness depends on your current balance and whether you received a Pell Grant during your education. If you received a Pell Grant, you could qualify for up to $20,000 in debt relief. If you did not receive a Pell Grant, you could qualify for up to $10,000 in forgiveness.

If you meet the eligibility requirements and your current loan balance is below the $10,000 or $20,000 maximum for which you qualify, your entire balance would be forgiven. For example, if you owe $7,000 and you qualify for up to $10,000, the entire $7,000 balance would be forgiven.

Refunds of Payments Made During COVID-19 Forbearance

In most cases, the loan forgiveness program does not provide reimbursement of payments you made in the past. However, there is a caveat if you made payments during the COVID-19 forbearance period. If your loan balance is below the forgiveness amount and you made payments between March 13, 2020, and December 31, 2022, you could be eligible for reimbursement of those payments.

For example, if you qualify for $10,000 in forgiveness, your current balance is $9,500, and you made $1,000 in payments during the COVID-19 forbearance, you could be eligible for a $500 refund in addition to having the $9,500 loan amount forgiven. No additional action is required for reimbursement. Just follow the instructions on the forgiveness application and the refund will be automatic if you qualify.

How will forgiveness be applied for those with multiple loans?

If you have multiple loans, the order of their forgiveness can be an important factor to consider. If you have any loans currently in default, those will be forgiven first. Specifically, Department of Education loans in default will be forgiven first, then any commercial FEEL loans that are in default. After loans in default, debt relief will be applied to non-defaulted direct and FEEL loans. Finally, any remaining forgiveness amount will be applied to non-defaulted Perkins loans.

If you have multiple loans of the same type, forgiveness will apply to those with the highest interest rate first. If the interest rates on your loans are also the same, unsubsidized loans will be forgiven before subsidized. If all those factors are the same, the most recent loans will be forgiven first.

Will student loan forgiveness be taxable?

Student loan forgiveness will not be taxed as income at the federal level. However, some states may tax the debt relief. The states that could or will tax student loan forgiveness include Arkansas, Indiana, Minnesota, Mississippi, North Carolina, and Wisconsin. If you live in one of these states, speak with your financial advisor or tax advisor to discuss your specific situation.

How to Apply for Student Loan Forgiveness

You must apply to see the benefits of student loan forgiveness. The online application is available now. If you can’t complete your application online, a paper version will be released soon but is not yet available. Whether you decide to apply online or on paper, you must submit your application before December 31, 2023.

The initial application is simple and should only take about five minutes. It doesn’t require you to upload any documentation or even sign into your account. If your income information is already on file, your debt relief will be automatic. If any additional information is needed to verify your income or student loan balances, you will be contacted by email with instructions.

It could be helpful to discuss your situation with an experienced financial advisor – especially if you live in a state that could tax your forgiveness. Your advisor can help you determine your eligibility, discuss any tax liability you could incur, and forecast how student loan forgiveness could impact your retirement plan.

Meet with an Advisor at Meld to Learn How Student Loan Forgiveness Could Impact Your Retirement Plan

The team of tax, legal, and investment professionals at Meld Financial has spent nearly 40 years helping our clients achieve their financial goals. Our unique wealth management platform, Financial Fingerprint®, is quick to assemble, easy to understand, and simple to modify as your circumstances change. With Financial Fingerprint®, you can determine how student loan forgiveness impacts your current financial position and your ability to reach your goals.

Contact us to learn more about Financial Fingerprint®.