If you have a mortgage, a child’s upcoming college, or a family that depends on your income, you could probably benefit from life insurance protection. This coverage helps replace your income and ensure your family is financially secure if you pass away unexpectedly.

While you may recognize the need for life insurance, there can still be challenges to obtaining it. The first of these is determining which type of policy matches your situation. If you choose the right plan, it will protect your family without straining your monthly budget.

The Basics of Life Insurance

Like other forms of insurance, life insurance typically requires monthly premium payments. These premiums are based on the amount of risk you pose – the likelihood of the policy paying your beneficiaries.

The insurance company typically determines your level of risk through underwriting. This process can include a review of your health records, family history, and even a physical examination. Typically, the amount of risk you pose increases as you get older or develop health problems. For this reason, it can be less expensive to buy life insurance when you are young and healthy, even if coverage will continue as you grow older.

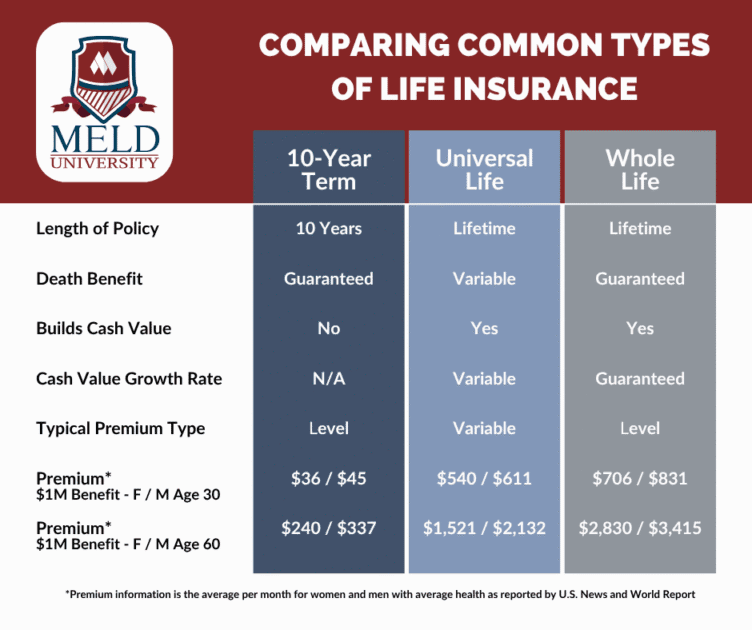

Another factor that determines the cost of life insurance is the type of policy you buy. There are two main options – term and permanent life insurance. Each of these has its own blend of costs, benefits, and drawbacks. The chart below summarizes these differences.

Term Life Insurance – What is it and who needs it?

Term life insurance provides temporary coverage, usually for a period of 10, 15, 20, or 30 years. If you have this type of policy, your family will only receive the payment if you die within the covered timeframe. On the other hand, if you survive past the expiration of the policy, your family does not receive the benefit.

These policies are intended to provide coverage when your family is most vulnerable. To illustrate, suppose you are 30 years old with limited savings, two small children, and a large mortgage. In this case, your family could be financially devastated by the loss of your income. A term life insurance policy can help your family pay off the mortgage, replace your lost income, and provide for your children in the case of an untimely death.

Due to the limited coverage period, term policies are typically much less expensive than permanent alternatives. For example, the average 30-year-old woman would pay just $36.16 per month for a $1 million 10-year term life insurance policy. A man who meets the same criteria would pay just $44.99 per month.1

To summarize, term life insurance policies offer a cost-effective way to protect your family when you need life insurance the most. The lower cost of premiums and the targeted coverage make term life insurance the preferred choice for most people.

Permanent Life Insurance – What is it and who needs it?

Permanent life insurance is lifelong coverage. It pays a benefit to your heirs no matter how long you’ve had the policy – though, there are sometimes exceptions if you die from certain causes within a short time after purchasing it.

This type of life insurance also builds cash value, which means you may be able to “cash out” your policy if needed. However, there can be steep surrender charges, and you could owe tax if you do this. Some types of permanent life insurance also include the option to use your cash value or part of your death benefit for long-term care costs during your life.

There are several sub-types of permanent life insurance, and each has a different way of calculating benefits and accumulating cash value. Some of the most common include:

- Whole Life. This type of life insurance typically offers afixed premium, a fixed death benefit, and a fixed return on cash value. Because this type of policy includes so many guarantees, it is usually the most expensive type of life insurance.

- Universal Life. This type of life insurance typically offers an adjustable premium which increases over time. Both the cash value and death benefit grow based on market interest rates.

- Variable Life. This type of life insurance typically offers a fixed premium and a fixed death benefit, but the cash value varies based on the performance of underlying investments.

Permanent life insurance is often very expensive compared to term insurance options. For example, a 30-year-old woman with average health would pay $705.94 per month for a $1 million whole life insurance policy. A man who meets the same criteria would pay $831.46.1

These plans can also offer riders which allow you to purchase additional coverage for specific situations. Riders often add even more cost to a permanent life insurance policy, so pay attention to the associated premium changes before you purchase. The high cost makes this type of life insurance inaccessible – and inappropriate – for most people.

Before you purchase a life insurance policy, it is important to consider how much coverage is right for your family, the monthly cost of the plan, and the benefits you could receive. These decisions can have a significant impact on your family’s financial health both during your life and in death. For these reasons, it is important to discuss your life insurance needs with an experienced financial advisor before committing to a policy.

Discuss Your Life Insurance Needs with the Meld Financial Team

At Meld Financial, our team of tax, legal, and investment professionals can help you determine if you need life insurance and how it fits into your overall financial plan. We can also help you choose the right policy to secure your family’s financial future without compromising your monthly budget. We do this through our comprehensive wealth management program, Financial Fingerprint®.

Developing your Financial Fingerprint® begins with a review of your financial situation and goals. Then, our advisors devise custom strategies to help achieve your goals while ensuring that your family is protected in the present.

Contact us to get started.

1The premium information in this article is courtesy of U.S. News and World Report. Premiums are the average monthly cost for men and women with average health.