A 401(k) or other employer-sponsored retirement plan may play a central role in your retirement plan – especially if you work for a company that offers matching contributions. Maximizing your deposits to this type of account helps you get the most “free money” from your employer, save on taxes, and grow your funds throughout your working years.

The IRS reviews inflation data each year to determine the maximum contribution limit for 401(k)s and other similar types of plans. They recently announced the 2026 contribution limits, which were raised to allow you to save more than previous years.

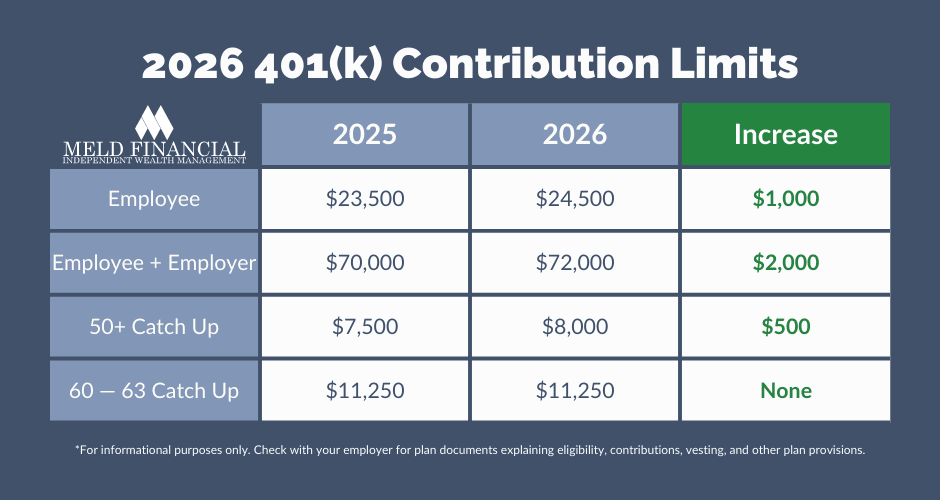

401(k) Contribution Limits in 2026

Contributions to 401(k) plans are subject to two limits – an overall maximum, and a limit on salary deferrals. The limits for each will rise in 2026.

Salary deferrals, in the context of your 401(k), are the amount that you contribute from each paycheck. These contributions are limited to $24,500 in 2026, which is a $1,000 increase from the 2025 limit of $23,500.

The total allowable contribution to your plan is $72,000 in 2025, and that figure includes the sum of salary deferrals, employer matching, and other employer contributions. This amount is $2,000 higher than the 2025 limit of $70,000.

If you are age 50 or older, you can make “catch-up” contributions in addition to the standard limits – if your employer offers this feature. The catch-up limit is an additional $8,000 if you are over the age of 50, and this represents a $500 increase from the 2025 limit of $7,500. For those between the ages of 60 and 63, the catchup limit is increased to $11,250 – the same limit as 2025.

The table below summarizes the change in contribution limits for 401(k) plans from 2025 to 2026.

403(b) and Government 457 Plan Contribution Limits in 2026

If you work for a nonprofit or government entity, you could have a 403(b), Thrift Savings Plan, or government 457 retirement plan. These plan types have the same contribution limits as 401(k) plans, so they will also rise in 2026.

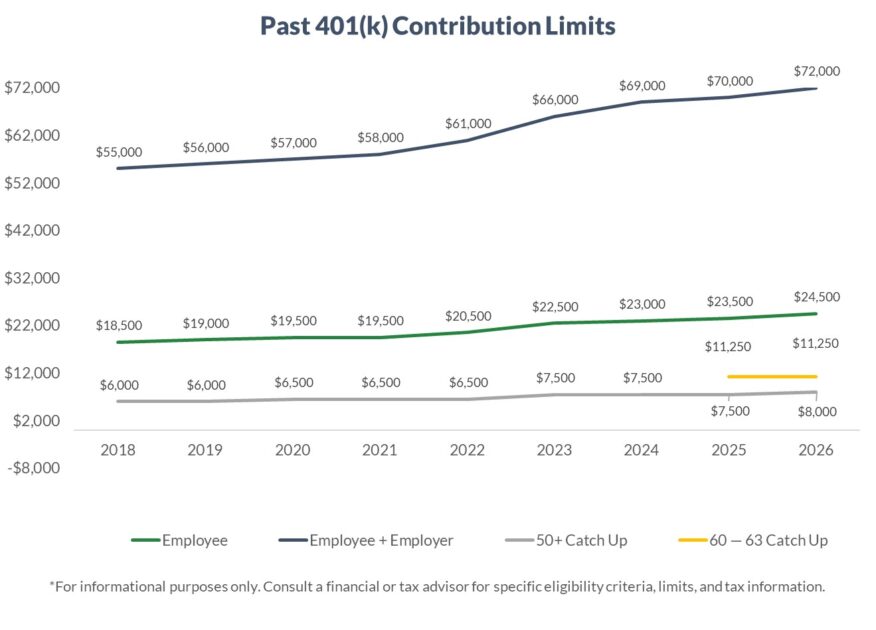

Past 401(k) Contribution Limits

Since contribution limits are adjusted each year to account for inflation, it stands to reason that these limits have risen steadily over the past several years. The chart below shows the changes to contribution limits since 2018.

You Can Still Contribute For 2025

You can contribute to a 401(k) up until December 31st, so there is still time to maximize your 2025 contributions. This year, the limits are $23,500 for salary deferrals and $70,000 total. If you are over age 50, you can contribute an additional $7,500 as a catch-up contribution or $11,250 if you are between ages 60 and 63. Find the full details on 2025 contribution limits in our article 401(k) Contribution Limits in 2025.

Tips to Grow Your 401(k) in 2026

Maximizing your 401(k) contributions is an excellent start, but you also need to refine your retirement plan to include investments, taxes, and the timing of your contributions to get the full benefit from your plan. The following tips will guide you through the tasks you need to complete to set yourself up for retirement success.

1. Increase Contributions As Soon As Possible

Few employer-sponsored plans automatically adjust to new contribution limits, so you will likely need to manually update your automatic contributions. Do this before the first pay period in January to take advantage of compounding – allowing your investments the most time to work throughout the year.

2. Get Your Employer Match

Even if you aren’t financially able to contribute the maximum to your 401(k), add enough money to the account to get your full employer match. This amount varies based on specific company rules but is often between 3 and 6% of your salary.

As you plan your contributions, keep in mind that some employers only match in the months you contribute, up to a prorated maximum. This means you could miss some matching contributions if you front-load your 401(k) in the first few months of the year. Your Human Resources department and plan document are excellent resources to determine the method in which your company processes matching contributions, and whether this unique situation applies to you.

3. Partner With a Financial Advisor to Review Investments

Once you’ve planned your contributions, you also need to evaluate your investment selections. The funds you choose can have a significant impact on the risk and potential return of your portfolio.

An experienced financial advisor can help you analyze the investments available in your plan and choose the ones that match your ideal balance between risk and reward. They can also evaluate your full financial picture and help you make the tough decisions that promote retirement success.

Optimize Your 401(k) Strategy with Meld Financial

At Meld Financial, our team of tax, legal, and investment professionals can help you optimize 401(k) contributions and investments. We have spent over four decades helping clients prepare for retirement, and we have gained the experience necessary to help you reach your goals.

Our unique approach to retirement planning centers around a wealth management program called Financial Fingerprint®. We developed this program in-house to bring together the most important aspects of your financial life in a simple plan that grows with you.

To learn more about Financial Fingerprint® and discuss your personal situation, contact a member of our team today.