Individual Retirement Accounts [IRAs] – referred to as retirement ‘arrangements’ by the IRS – can be an easy, flexible way to increase retirement savings and lower your tax bill. This year, you can contribute more to these types of plans. Incorporate the new, higher limits into your financial plan as soon as possible to make the most of these nimble investment vehicles.

Traditional and Roth IRA Limits in 2023

For tax year 2023, you can contribute up to $6,500 to a Traditional or Roth IRA (or a combination of the two) – a $500 increase from the 2022 limit. If you’re 50 or older, you can also make up to $1,000 in catch-up contributions. The catch-up contribution limit was not increased for 2023.

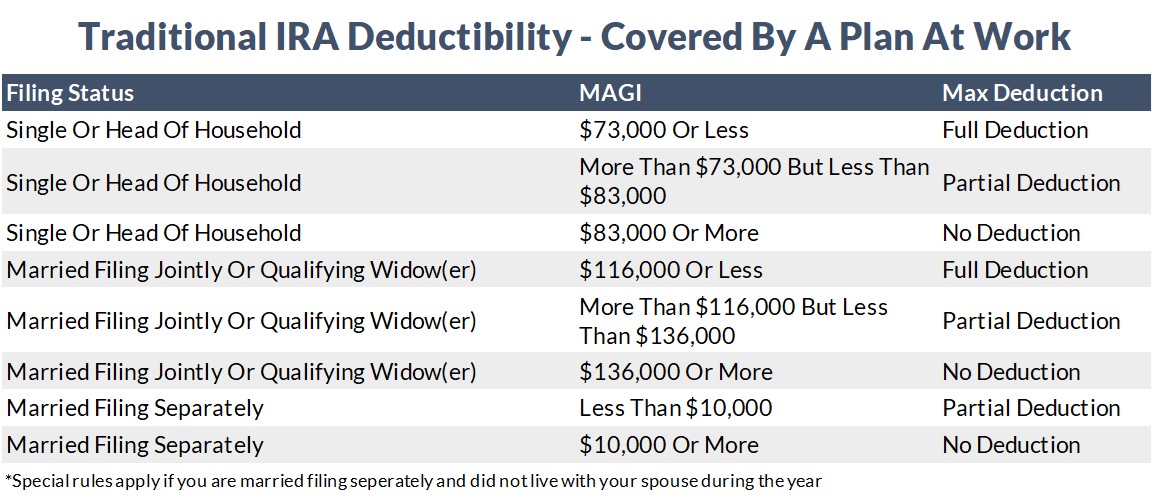

Traditional IRA Deductibility in 2023

Some contributions to Traditional IRAs are tax deductible. However, deductibility is dependent on filing status, income, and whether you or your spouse are covered by a retirement plan at work. For tax year 2023, the deductibility limits were increased to account for inflation. See the tables below to determine if you are eligible to deduct Traditional IRA contributions.

Roth IRA Income Limits in 2023

Unlike Traditional IRAs, Roth IRAs don’t save you money on your taxes in the current year. However, your investments grow and can be withdrawn tax free in retirement if you meet certain criteria. The amount you can contribute to a Roth IRA depends on your filing status and income. These amounts were increased for tax year 2023. See the table below to determine if you are eligible to contribute to a Roth IRA.

If your income is above the limit, you may still be able to add funds to a Roth IRA using a strategy called back-door Roth contributions. There are important caveats to using this method, so discuss your options with an experienced financial advisor.

SEP IRA Contribution Limits in 2023

If you are self-employed, you may have a SEP IRA. These plans allow you to make employer contributions to your retirement. For tax year 2023, you can contribute up to $66,000 to this type of plan – a $5,000 increase from 2022’s limit. However, it is important to remember that contributions are still limited to 25% of compensation. Unlike most other employer sponsored retirement plans, SEP IRAs do not allow you to contribute as an individual. For this reason, there is no age-based catch-up contribution. Depending on your situation, you may be able to contribute to a Traditional or Roth IRA as an individual in addition to employer SEP IRA contributions. Discuss this option with an experienced financial advisor.

SIMPLE IRA Contribution Limits in 2023

If your employer offers a SIMPLE IRA, you can contribute up to $15,500 in 2023 – a $1,500 increase from the 2022 limit. If you are 50 or older, you can also make catch-up contributions. These are limited to $3,500 for tax year 2023 – a $500 increase from the previous year. With a SIMPLE IRA, your employer can either match contributions up to 3% of your salary or offer a 2% nonelective contribution. If your company uses the nonelective contribution method, they will add 2% of your compensation up to the salary cap of $330,000. This limit was increased from $305,000 in 2022.

Incorporate The New IRA Limits into Your Financial Plan

This January, incorporate the new, higher IRA limits into your retirement savings strategy. To do this, work with an experienced financial advisor to make the following changes:

Update Your Contribution Amounts

Whether you contribute to an individual IRA or participate in an employer sponsored IRA, you will likely need to update your contributions to reflect the higher limits. Most IRAs won’t automatically update to the new maximum, so you’ll have to make the change manually. If you don’t increase your contributions promptly, you could miss the opportunity to add to your savings and reduce your taxes.

Review Your Retirement Savings Strategy with An Experienced Financial Advisor

An experienced financial advisor can help you determine the optimal amount to save in an IRA each year and balance IRA holdings with other retirement savings vehicles – like 401(k)s. An advisor can also help weigh the tax implications of Traditional and Roth investments to determine the most advantageous option for your situation.

In addition to determining the right type of IRA, an experienced financial partner can help you choose investments that match your unique goals and risk tolerance. With a comprehensive financial plan and an experienced advisor, you can make the most of IRAs.

Optimize Your Retirement Strategy with Meld Financial

At Meld Financial, our team of tax, legal, and investment professionals will develop a retirement plan unique to your specific situation. Our proprietary wealth management program, Financial Fingerprint®, is quick to assemble, easy to understand, and simple to modify as your circumstances change. This comprehensive plan considers all retirement accounts – including your IRAs – and how they work together to help you achieve retirement goals.

Contact us today to get started.