Individual Retirement Accounts – better known as IRAs – are a popular tool for individuals looking to optimize their retirement savings and tax burden. These accounts have annual deposit limits and rules surrounding which people can contribute each year.

The IRS updates the applicable limits each year to account for inflation. They recently announced the new limits for 2026, and most people will be able to contribute more next year than in previous years.

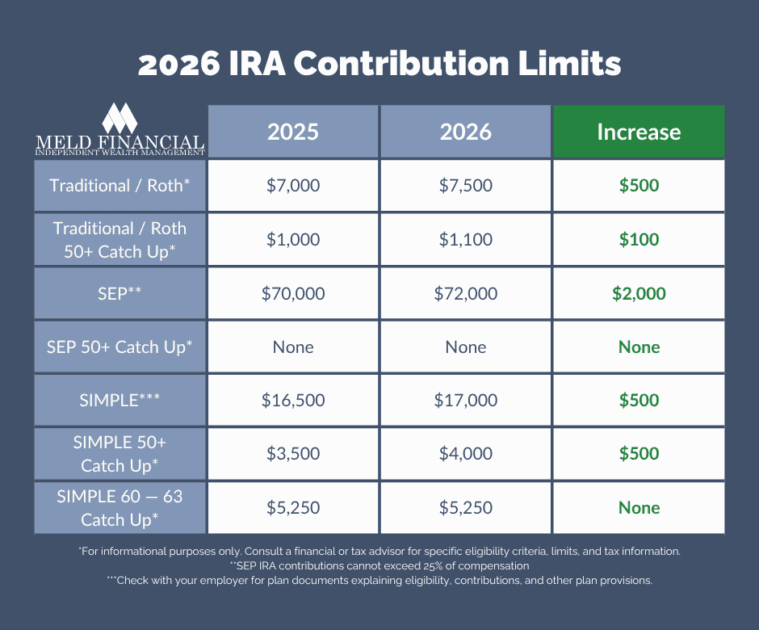

IRA Contribution Limits for 2026

The most common types of IRAs are Traditional and Roth, which are not tied to a particular employer. Other types, including SEP and SIMPLE IRAs, are employer-sponsored. Each of these plan types is subject to different contribution limits, and all of them will rise in 2026.

Traditional and Roth IRA Contribution Limits

Next year, the annual contribution limit for Traditional and Roth IRAs will rise to $7,500 from $7,000 per year in 2025. This limit applies to your total contributions to a Traditional IRA, Roth IRA, or a combination of the two.

If you are age 50 or older, you can also make a “catch-up” contribution – an extra incentive for those nearing retirement to increase their savings. The catch-up contribution limit will increase to $1,100 from $1,000 in 2025, and it brings the total allowable contribution to $8,600 for those in the over 50 age group.

SIMPLE IRA Contribution Limits

The maximum you can add to a SIMPLE IRA in 2026 is $17,000, a $500 increase from the 2025 limit of $16,500. If you are over age 50, you’ll also be able to contribute an additional $4,000 catch-up contribution, $500 more than in 2025. SIMPLE IRAs are also subject to a special catch-up limit of $5,250 for those aged 60 through 63.

SEP IRA Contribution Limits

For self-employed individuals, a SEP IRA can be a powerful way to save for retirement because it allows you to contribute to your retirement on behalf of your business. Contribution limits for these accounts will increase to $72,000 – $2,000 higher than 2025.

The table below provides a summary of the change in IRA contribution limits from 2025 to 2026.

Past IRA Contribution Limits

Since the IRS uses inflation data to inform IRA contribution limits, the limits tend to follow the path of inflation. The high inflation rate in the post-COVID era led to several years of rapid increases in contribution limits, which brought them from $6,000 in 2020 to $7,500 in 2026. The Consumer Price Index rose by 25.1% from January 2020 to September 2025, the latest month for which data is available, closely matching the 25% increase in contribution limits shown below.

Traditional and Roth IRA Contribution Limits in 2025

As you plan for the 2026 contribution limits, also keep in mind that you may still be able to contribute under the current limits. Traditional and Roth IRA contributions for 2025 can be made until the tax filing deadline – Wednesday, April 15th, 2026.

The 2025 contribution limits are $7,000 for Traditional and Roth IRAs, and the catch-up contribution limit for those age 50 or older is $1,000. These limits are subject to Traditional IRA deductibility rules and income limits for Roth IRAs, and you can find the details for these limitations in our article IRA Contribution Limits in 2025.

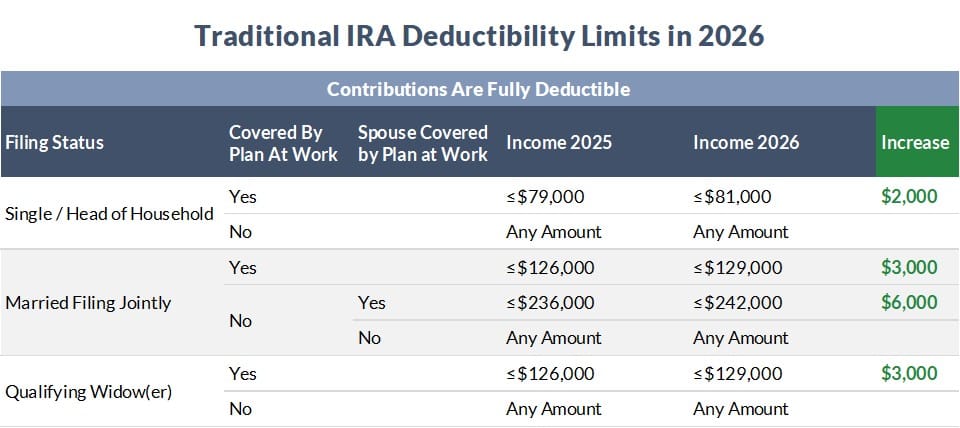

Traditional IRA Deductibility Limits in 2026

Most people who choose a Traditional IRA over a Roth alternative do so when they want to receive an immediate tax benefit. However, not everyone qualifies for these benefits because the IRS limits which people can deduct their contributions.

These deductibility limits are based on tax filing status, income, and coverage by an employer-sponsored retirement plan. The table below summarizes the updated rules for 2026.

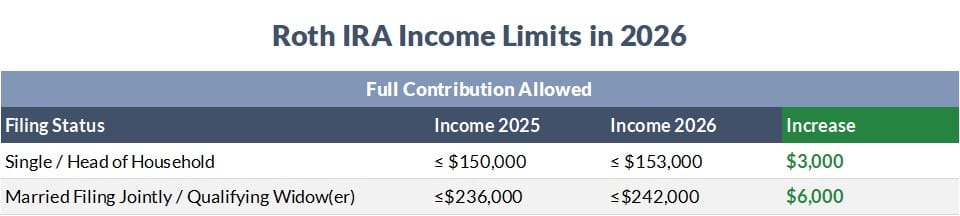

Roth IRA Income Limits in 2026

Unlike Traditional IRAs, contributions to a Roth IRA are not tax deductible, so there are no deductibility limits. Instead, Roth accounts provide tax benefits during retirement. These benefits are attractive for many high earners, but the IRS only allows people with income below certain limits to contribute to this type of account.

The 2026 Roth IRA income limits were adjusted for inflation, and the table below summarizes the new limits.

If your income is above the applicable limit, you may be able to contribute to a Roth IRA using a back-door contribution strategy. However, this strategy has important caveats, so be sure to discuss your situation with an experienced financial advisor before implementing it.

Adjust Your Financial Plan for New IRA Limits

If you use an automatic contribution account feature to maximize your IRA savings, you will likely need to update the settings of your account to reflect the new limits. Most plans do not automatically adjust each year, and you’ll need to specify a dollar amount to contribute each month.

As you adjust your account to reflect the 2026 limits, take the time to review your investment strategy and rebalance your account to match your ideal portfolio mix. An experienced financial advisor can make this process seamless, handling account updates and investments to match your goals.

Maximize Your IRA Savings with Meld Financial

At Meld Financial, our team of professionals can help you determine the optimal amount to save in an IRA, and which type of account suits your needs. We also take the work of investing off your plate – including updating automatic contributions and choosing appropriate investments to help grow your funds.

Our comprehensive financial plan – Financial Fingerprint® – is the foundation of our wealth management program. It brings together the most important aspects of your financial life in one easy-to-understand plan that adapts to your changing circumstances.

To discuss your retirement strategy and get started with Financial Fingerprint®, contact us today.