Social Security benefits have been an important source of income for Americans since the Great Depression. For the first several decades after the program was implemented, these benefits were exempt from taxation. Then, a 1983 law made benefits subject to income tax for some individuals with other sources of retirement income. A second legal change in 1993 raised the amount of tax that high earners pay on their Social Security benefits.

Today, about half of Social Security recipients owe tax on part of their benefits. To determine if you will be among this group, you first need to calculate your Provisional Income. This figure is a specialized calculation that is only used to determine how much of your Social Security benefits are taxable. By understanding how to calculate this figure, you can better plan for taxes in retirement and work to minimize these expenses.

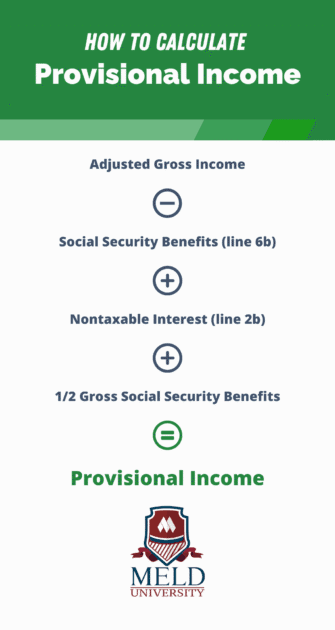

How to Calculate Provisional Income

The calculation for provisional income is rather simple. Start with your adjusted gross income [AGI] from line 11 of your 1040 tax form, then exclude Social Security benefits (line 6b). This figure could include wages, self-employment income, pension benefits, dividends, interest, or any other form of taxable income.

Next, add interest income that is nontaxable at the federal level (line 2b). One of the most common examples of this interest is income from municipal bonds.

Finally, add one half of the gross Social Security benefits from your Form SAA-1099. Keep in mind, married couples should include income from both spouses. When this calculation is complete, the result is what the Social Security Administration calls “combined income” or Provisional Income.

How Provisional Income Affects Taxation

Similar to the progressive income tax system, there are thresholds for Provisional Income that affect the taxation of Social Security benefits. These magic numbers are $25,000 and $34,000 for individuals, and $32,000 and $44,000 for joint filers.

Reaching either of those two income levels greatly increases the tax exposure of an individual’s or couple’s Social Security benefits. The respective tax burdens are:

- 0% for individuals who have Provisional Income below $25,000 ($32,000 for joint filers)

- up to 50% for individuals who have Provisional Income between $25,000 and $34,000 ($32,000 to $44,000 for joint filers)

- up to 85% for individuals who have Provisional Income above $34,000 ($44,000 for joint filers)

Unlike most types of U.S. taxation, the provisional income levels are not adjusted for inflation each year. They only change when Congress acts to raise them. For this reason, your tax burden could change from year to year as your benefits rise due to Cost-of-Living Adjustments or when you pull more money from retirement accounts to cover rising bills.

How to Calculate Your Tax Burden for Social Security Income

Calculating your individual tax burden for Social Security income is a bit more involved than determining your Provisional Income. For those in the middle category listed above, taxable benefits are the lesser of:

- 50% of the annual Social Security benefits received

- 50% of the filer’s Provisional Income above the threshold

Detailed examples on how to calculate the tax burden for Social Security income can be found on the IRS website. For more personalized guidance, work with a financial advisor who has vast experience with Social Security and tax planning.

Using Your Provisional Income to Minimize Your Tax Burden

Income taxes can greatly reduce your retirement income, and, in some cases, a high tax burden can keep you from living the retirement of your dreams. That’s why it is important to have a plan in place for managing taxes during your retirement years.

The first step in an effective tax plan is to forecast your future tax burden, starting with your Provisional Income. Then, you can work with a group of experienced financial professionals to find ways to minimize the amount you owe.

Work with Meld Financial to Optimize Taxes in Retirement

At Meld Financial, we can help you determine how taxes fit into your retirement plan. Then, our team of tax, legal, and investment professionals can offer solutions for optimizing your tax burden that are tailored to your specific situation.

In addition to helping you minimize taxes, our financial planners can leverage their vast experience to develop your Financial Fingerprint®. This comprehensive wealth management program brings together the most important aspects of your financial situation in one easy-to-understand plan.

With your Financial Fingerprint®, and an ongoing relationship with our team of experienced financial advisors, you can turn your retirement dreams into a reality. Contact us today to get started with Financial Fingerprint®.