Health Savings Accounts [HSAs] are one of the only types of investment accounts that provide triple tax advantages. That means you receive a deduction for contributions, you won’t owe taxes on earnings each year, and your withdrawals are tax free if you meet certain criteria.

With so many benefits to this type of account, it stands to reason that the IRS must impose limits on how much each person can contribute. Fortunately, those limits are increasing for 2026 to account for inflation, so you will be able to add even more money next year.

HSA Contribution Limits Will Rise in 2026

The IRS reevaluates contribution limits for investment accounts each year to include the impact of rising costs. The agency recently announced that HSA limits will rise for both individual and family plans in 2026.1

Individual HSA Contribution Limits in 2026

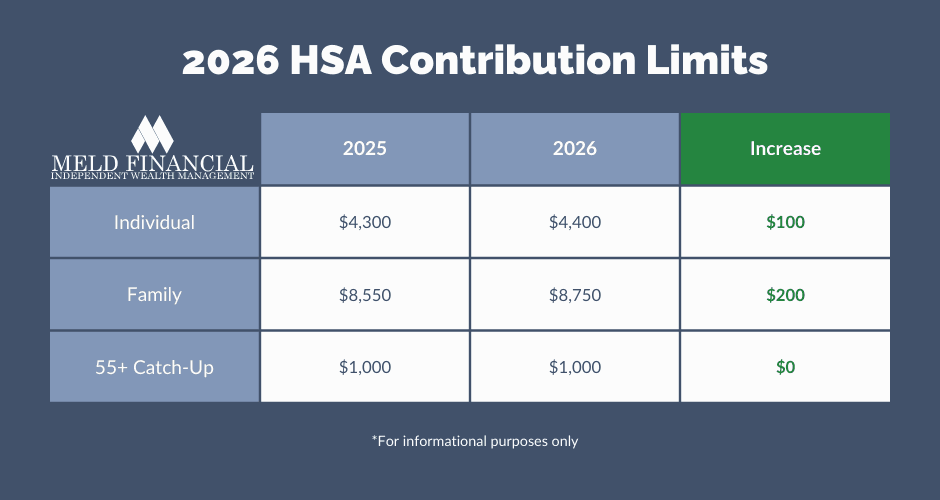

Individuals with high-deductible health care plans will be able to contribute $4,400 to an HSA in 2026. This marks an increase of $100 from the 2025 limit, and the new, higher limit will help these individuals cover the rising costs of medical care.

Family HSA Contribution Limits in 2026

Contribution limits for families with high-deductible health plans will also rise next year. This limit will increase by $200 from $8,550 in 2025 to $8,750 in 2026.

HSA Catch-Up Contribution Limits in 2026

Funds in an HSA do not expire at the end of each year and can be an excellent way to cover health costs in retirement. The IRS recognizes this benefit and allows a “catch-up” contribution for people age 55 and older. This annual limit will remain at $1,000 per year in 2026, and it applies in addition to the standard individual or family limit.

See the table below for a summary of HSA contribution limits in 2026.

Past HSA Contribution Limits

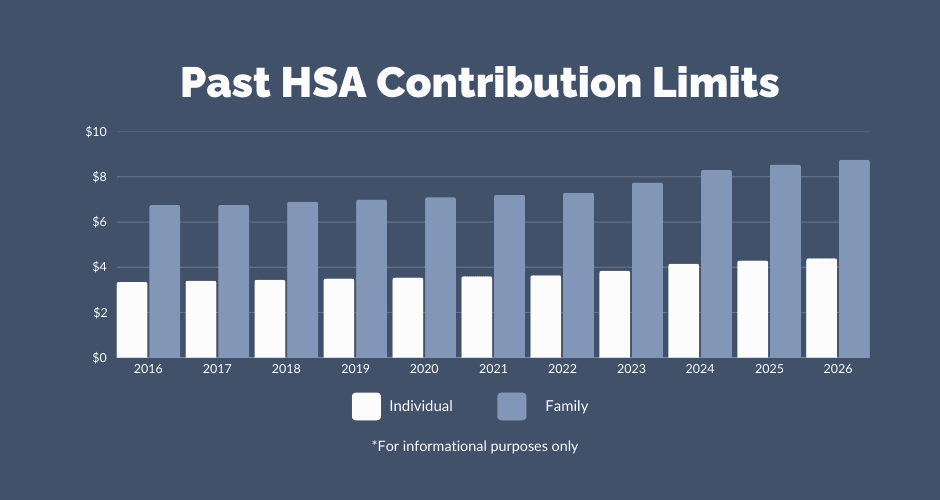

The IRS has raised the HSA contribution limit every year for the past decade. The increases have totaled about 31% and brought the individual limit from $3,550 in 2016 to $4,400 in 2026.

As the graph below shows, annual changes to the limits were particularly large in 2023 and 2024 – years when the inflation rate was historically high. Increases in 2025 and 2026 were more modest, but still above the average annual increase over the past decade.

Who Can Contribute to an HSA?

With the attractive tax benefits and new, higher contribution limits, it may seem obvious that everyone should open an HSA. However, these accounts are restricted to certain people with specific types of health care plans.

You Must Have a HDHP To Participate in an HSA

To be eligible to contribute to an HSA, you must have a high-deductible health plan [HDHP]. These plans are defined by the IRS as having an annual deductible of at least $1,700 for an individual or $3,400 for a family. High-deductible plans also have maximum out-of-pocket expenses of $8,500 for an individual or $17,000 for a family.

The One Big, Beautiful Bill Act also opened HSA eligibility to people with Bronze or Catastrophic Affordable Care Act plans. This change takes effect on January 1, 2026, so if you have this type of plan, you’ll be eligible to contribute next year.

If you’re unsure whether your health care plan matches these criteria, the Human Resources department at your company or the broker who sold you the plan can be valuable sources of information. You can also contact an experienced financial advisor to review your coverage and eligibility.

HSA Contributions Are Prorated If You Have a HDHP for a Partial Year

You can contribute to an HSA if you have HDHP coverage at any point during the year. However, your maximum contribution is prorated based on the number of months you have the plan if you only have it for part of the year.

Your HDHP Must Be Your Only Source of Health Insurance

One of the most common issues with HSAs arises from the rule stating that your HDHP must be your only source of health insurance when contributing to an HSA. This rule doesn’t apply to special types of coverage – like dental and vision insurance – but it does apply to Medicare.

In short, you cannot contribute to an HSA if you are enrolled in Medicare. Due to the backdating of benefits, you should stop contributing to an HSA before the month of your 65th birthday or 6 months before starting Medicare if you are enrolling after age 65. Our article, How Medicare Impacts HSA Contributions, provides a more detailed explanation of this topic.

While you must stop HSA contributions before you enroll in Medicare, you can use HSA funds to cover some Medicare costs – like Part A and B premiums as well as Medicare Advantage premiums. However, Medigap premiums do not qualify for tax-free withdrawals from an HSA.

The One Big, Beautiful Bill Act also clarified that insurance plans that offer 100% coverage for telehealth services still qualify as HDHP plans if they meet the other criteria. Additionally, the bill stated that HDHP participants can enroll in Direct Primary Care arrangements without impacting their eligibility for an HSA. These clarifications removed some of ambiguity surrounding HSA eligibility.

HSAs are an important source of tax advantages as well as an excellent place to set aside funds to cover future medical costs. These accounts can even be an important part of your retirement plan when used correctly. Work with an experienced financial advisor to determine if you’re eligible to contribute and how you can use this type of account to your advantage.

Plan Your HSA Contributions with Meld Financial

At Meld Financial, our experienced team can help you determine if you are eligible for an HSA and how much you should contribute. We can also help you determine how this type of account fits into your overall financial strategy and your retirement plan.

Our financial planning process centers around a comprehensive program we call Financial Fingerprint®. This nimble plan brings together the most important aspects of your financial picture and adapts to changing circumstances throughout your life.

To learn more about Financial Fingerprint® or discuss your personal situation, contact a member of our team today.

Sources:

1 Internal Revenue Service. (2025, May 5). Revenue Procedure 2025-19.