Medigap plans can provide crucial coverage for healthcare during retirement, but the monthly premiums for these plans can be confusing, at best. One of the most important things you need to consider when comparing these plans is the way that they determine your premium.

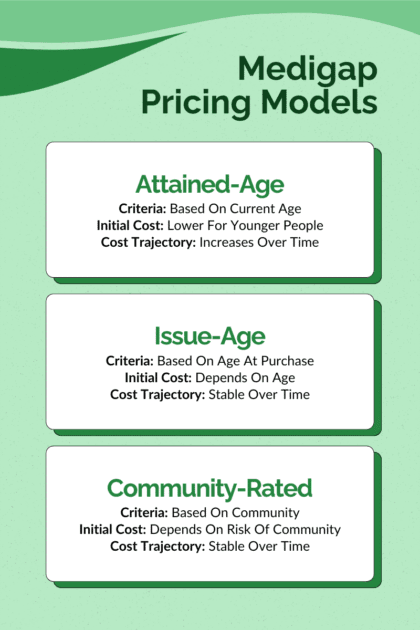

There are three main ways that insurance companies can determine your monthly premium – attained-age, issue-age, and community-rated. Understanding these terms can help you keep your costs manageable early in retirement and avoid unwelcome surprises later in life.

Attained-Age: Premium Increases Over Time

When premiums are calculated using the attained-age method, they are based on your current age. This means your monthly premium will typically increase as you get older, with annual adjustments occurring each year in the month of your birthday.

Some beneficiaries with attained-age plans are surprised to learn that their premiums increase during the month of their birthday, rather than on January 1st when most Medicare changes occur. Awareness of this possibility is crucial to maintaining an accurate budget if you choose this type of plan.

While a lower initial cost can be appealing, it is important to consider how increasing premiums over time will impact your budget as you age. These age-based increases occur on top of any inflation adjustments or cost changes that insurers put in place to account for rising healthcare costs. Therefore, your premiums could rise faster than the inflation rate, your Social Security Cost-of-Living adjustments, or the value of your portfolio.

Additionally, switching Medigap plans could require you to go through medical underwriting. This process takes your health situation into account when determining if you qualify for coverage and how much your premiums will be. For this reason, you may have trouble switching from an attained-age plan to another type of plan later in life if your premiums reach an unmanageable level. For this reason, be sure to carefully evaluate your current premiums and your expected future premiums before purchasing an attained-age plan.

An Example of Attained-Age Medigap Premiums

John is 65 years old when he purchases a Medigap policy. His initial monthly premium is $140. The following year, he reaches age 66, and his monthly premium increases to $146. The year after that, it increases to $152 per month, and it continues to climb each year.

Issue-Age Plans Allow You To “Lock In” Your Rate Early

Issue-age plans determine your premium using your age when you first purchase the policy. Then, your premium is not increased due to age in subsequent years. However, your monthly cost could still rise due to changes the insurer implements – like increasing premiums across all policyholders to account for rising healthcare costs or inflation.

These plans are generally most beneficial for people who are buying their policy at an early age, because they can “lock in” a lower premium than they would pay if they purchased the same plan later. On the other hand, the initial monthly payments may be higher than an attained-age plan for beneficiaries buying a policy at an early age.

An Example of Issue-Age Premiums

John is age 65 when he buys an issue-age Medigap policy with a monthly premium of $165. His premium does not change based on age moving forward. Jane buys the same plan as John, but she is 72 years old. Her premium is $195 due to her age. Like John, Jane’s premium doesn’t increase over time due to her age.

Everyone Pays the Same with Community-Rated Plans

Community-rated plans are unique because age doesn’t influence your premium. Instead, everyone in a specific geographic area pays the same premium for a Medigap plan.

Community-rated plans offer stable premiums over time like issue-age plans. However, community-rated plans may offer more favorable pricing than issue-age for people who are buying a new policy later in their retirement.

An Example of Community-Rated Medigap Premiums

John buys a community-rated plan at age 65 and his monthly premium is $185. Jane buys the same plan at age 72, and her premium is also $185 per month because age isn’t a factor in the pricing.

The pricing models for Medigap plans can be confusing. Refer to the following graphic for a simple comparison.

Your State Can Determine Which Types of Plans Are Available

Most states are “open choice,” meaning that insurance companies can use any of these methods to determine premiums. However, some states have additional requirements or prohibitions that could impact your costs.

States With Community-Rated Mandates

Nine states require Medigap premiums to be community-rated for policyholders aged 65 or older. These are Arkansas, Connecticut, Idaho, Massachusetts, Maine, Minnesota, New York, Vermont, and Washington. If you live in one of these states, your Medigap premium will be the same as other community members, regardless of your age.

States That Prohibit Attained-Age

Four states permit issue-age rating methods but specifically prohibit attained-age rating systems. These states are Arizona, Florida, Georgia, and Missouri. In these states, you won’t have the option to secure lower premiums in the early years of your retirement.

Other Factors That Influence Your Medigap Premium

Outside of the age-based or community-rated type of plan you buy, other factors can also impact your monthly Medigap payments. Understanding these can help you better anticipate your costs.

- The Plan You Choose. Medigap plans are standardized, meaning Plan G from one insurer offers the same benefits as Plan G from another. However, the premiums, customer service, and extra perks – like gym memberships – vary between plans based on the coverage they provide.

- Inflation Adjustments and Annual Changes. Even with issue-age or community-rated plans, premiums are not entirely static. They can change each year to account for inflation, increased healthcare costs, or changes to the risk of the insurer. These adjustments are typically applied to all policyholders and are separate from age-related increases.

- Medical Underwriting. When you first become eligible for Medicare, you have an initial enrollment period, during which you are not subject to medical underwriting. However, if you apply for a policy outside of this period, you could be subject to underwriting. Insurers use this process to determine your risk of health issues, and the results of your underwriting could lead to higher premiums. The risk of higher premiums due to medical underwriting later in life makes it even more crucial to choose the correct plan the first time.

- Discounts for Lower Risk. Some insurance companies offer discounts to policyholders who are considered lower risk. For example, non-smokers might receive a discount.

- Other Discounts. Insurers may offer other discounts for bundling coverage, using automatic payments, or paying your premium annually.

Due to these factors, it is important to choose the right type of Medicare supplement plan early in your retirement and review your coverage and costs each year before open enrollment. The Medicare program is vast and can be confusing to navigate alone. Fortunately, an experienced financial advisor can offer impartial advice to help you get the coverage you need while minimizing your costs.

Manage Retirement Healthcare Costs with Meld Financial

At Meld Financial, our team of specialists can help you understand your Medicare options and how the cost of various types of coverage fits into your financial plan. Our holistic approach to financial planning includes your health coverage and many other aspects that are vital to your wellbeing.

To make this simple, we bring together the most important parts of your financial life into one easy-to-understand plan called Financial Fingerprint®. This nimble plan is the first step toward a financially secure retirement.

To learn more about Financial Fingerprint® or discuss your personal situation, contact a member of our team today.