Healthcare costs vary based on the health of the population and the corporate initiatives of service providers, so expenses of the Medicare program vary as well. The share of the total Medicare costs for which you are responsible includes monthly premiums, deductibles, and coinsurance – all of which can change year-to-year.

The Centers for Medicare & Medicaid Services [CMS] recalculate beneficiary costs each November, and they recently announced the new pricing for 2026. Overall, your costs for monthly premiums and services received could rise next year.

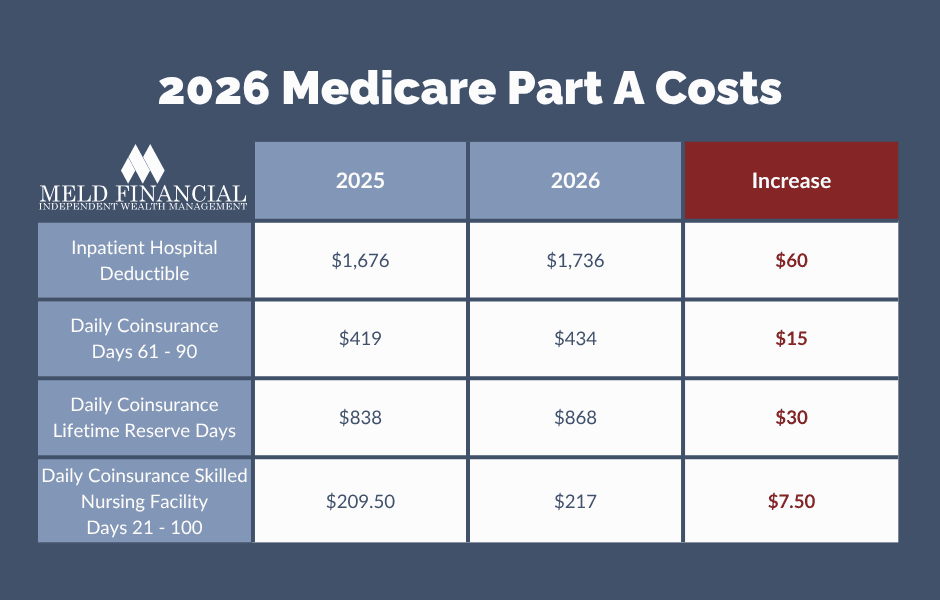

Medicare Part A Costs in 2026

Medicare Part A covers inpatient hospital stays, skilled nursing care, inpatient rehabilitation, and hospice. These services are available with no monthly premium for Americans who worked or whose spouse worked more than 40 quarters in a qualifying job. However, they are subject to deductibles and coinsurance for care received.

If you are admitted to the hospital in 2026, you will owe a Medicare Part A deductible of $1,736 – up by 3.6% from $1,676 in 2025. This cost applies for each spell of illness, and you could owe it multiple times throughout the year if you are admitted for different stays.

If a hospitalization lasts less than 60 days, the deductible is the only cost you will owe. On the other hand, if your stay lasts between 60 and 90 days, you will also owe a daily coinsurance amount of $434 – also up by 3.6% from $419 per day in 2025.

For stays longer than 90 days, you begin to use lifetime reserve days, which are subject to a higher coinsurance amount. This amount is $868 in 2026 – up by 3.6% from $838 per day in 2025.

You could also owe daily coinsurance of $217 for skilled nursing care required for more than 20 days but less than 100 days. Medicare does not cover skilled nursing care after 100 days.

The table below summarizes Medicare Part A costs in 2026.

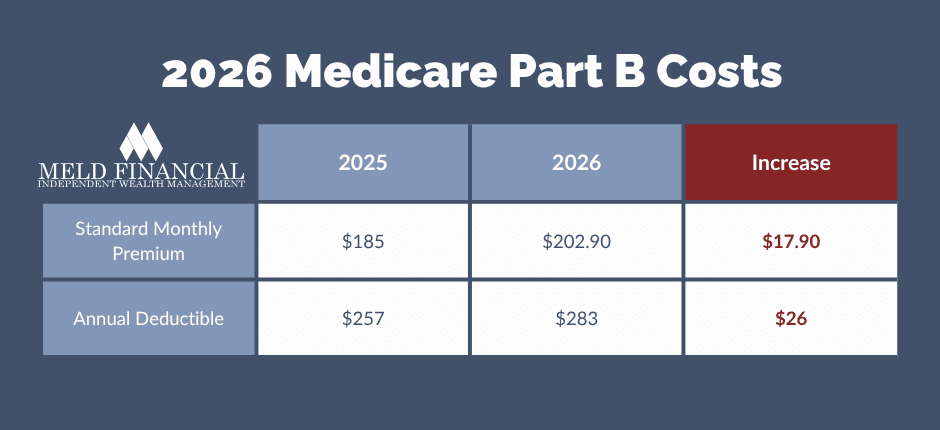

Medicare Part B Premiums in 2026

Medicare Part B covers outpatient medical care that is not covered by Part A, like doctor visits, outpatient hospital services, durable medical equipment, and some home health services. Unlike Part A, Part B requires a monthly premium of $202.90 in 2026. This amount increased much more substantially than Part A costs – rising by 9.7% from $185 in 2025.

In addition to the monthly premium, Part B is subject to an annual deductible. This amount will rise by 10.1% from $257 in 2025 to $283 in 2026.

The table below summarizes the changes to Part B costs.

The CMS announcement stated that the rise in Part B premiums and deductibles was due to projected price increases and utilization of services. The announcement also said that changes were consistent with historical experiences and would have been even higher without presidential action to reduce spending on skin substitutes.

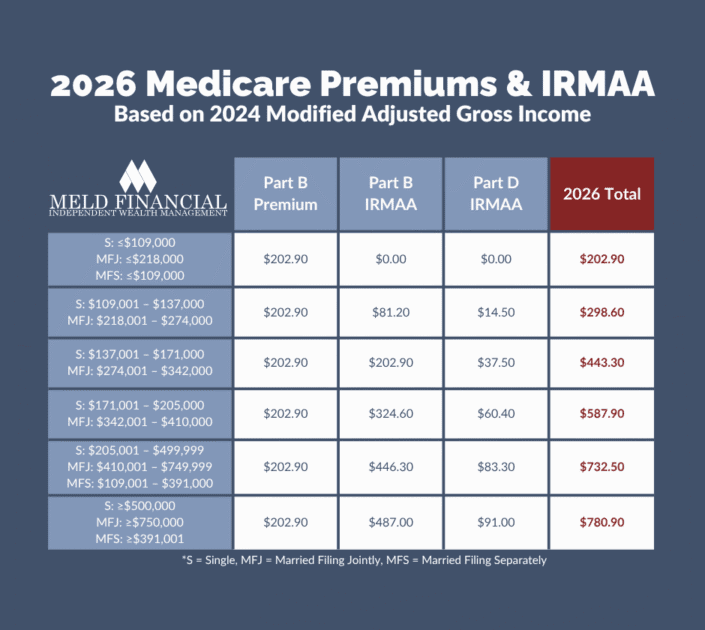

Medicare Part B and Part D IRMAA

High earners are subject to additional costs for Part B and Part D, known as the Income-Related Monthly Adjustment Amount [IRMAA]. It does not apply if your income is under $109,000 and you file taxes as Single or $218,000 for Married Filing Jointly.

If your income is above this amount, refer to the table below for a breakdown of your costs.

Like Medicare Part B premiums, Part B IRMAA rose by about 9.7% from 2025 to 2026. Part D IRMAA rose less substantially – increasing by an average of about 6% with each tier rising by a different percentage.

Your IRMAA is based on your Modified Adjusted Gross Income [MAGI] from 2024 – which is defined as Adjusted Gross Income from line 11 of your 1040 plus tax exempt interest on line 2a. If you’ve had a life-changing event since that time, like marriage, divorce, or loss of income due to work stoppage or reduction, you can appeal the additional cost. Contact an experienced financial advisor for more information on the appeal process or to discuss your Medicare coverage.

Review Your Medicare Coverage with Meld Financial

At Meld Financial, our team of professionals has the experience to answer your most pressing Medicare questions. We can help you estimate costs, review coverage each year, and choose the right supplement plan for your situation.

Throughout our decades of experience helping clients achieve their retirement goals, we developed a comprehensive wealth management program – Financial Fingerprint®. This nimble plan brings together the most important aspects of your financial life into one easy-to-understand plan that adapts to your changing circumstances.

To learn more about Financial Fingerprint® and get started, contact a member of our team today.