A large amount of cash may have been a reasonable, and even prudent, investment decision when yields were high. However, the Federal Reserve is now in the process of lowering interest rates, which could dramatically reduce the return on cash.

Before allowing the value of your funds to dwindle, understand how a substantial cash position impacts your overall investment strategy while interest rates are falling. Start by reviewing current yields and the real returns of your investments.

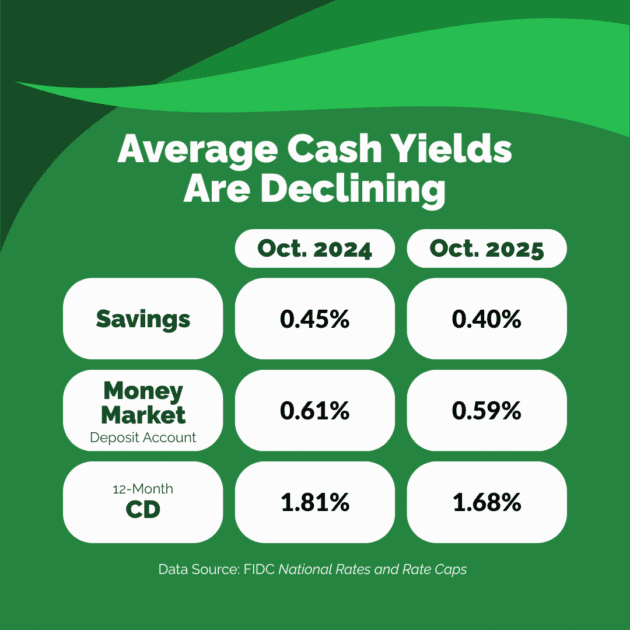

Returns on Cash Accounts Are Already Declining

The Fed began lowering interest rates in September 2024, and has lowered the Fed Funds Rate by a total of 1.50 percentage points since that time. Their most recent forecasts predict one additional rate cut before the end of the year.

The Fed Funds Rate most directly impacts banks who lend or borrow overnight, but some types of savings vehicles are also extremely sensitive to changes in this rate. In fact, average yields for most common bank accounts have already started to decline, including savings, money market deposit accounts, and Certificates of Deposit [CDs].

The table below summarizes the change in common bank account yields from October 2024 to October 2025. As you can see, average yields have declined by 0.05 percentage points for savings accounts, 0.02 percentage points for money market deposit accounts, and 0.13 percentage points for 12-month CDs.

In addition to cash accounts at banks, money market mutual funds have experienced a reduction in yield as interest rates have declined. Data from the SEC shows that yields for money market funds that include only government-issued securities fell from 5.38% in July 2024 to 4.37% in July 2025 – the most recent month for which data is available. Similarly, yields for money market funds that invest in both government and corporate securities fell from 5.49% to 4.48% over the same period.

Lower yields on cash diminishes your overall portfolio return and the amount of income you can expect to earn from these investments. In some cases, falling yields could even cause your real return to be negative.

Real Returns on Cash Investments May Be Negative as Rates Decline

The real return on an investment is the amount it earns minus the rate of inflation. This inflation-adjusted return could be negative if your cash grows more slowly than prices.

For example, the inflation rate in August 2025 was 2.9%, so if you owned a 12-month CD with a yield of 1.68% at that time, your annual real return was -1.22%. In other words, you lost 1.22% of your purchasing power.

Some types of cash investments currently have higher yields than the inflation rate, so they have a positive real return. However, continued interest rate cuts or increasing inflation could change this scenario.

Callable CDs: Another Threat to Your Real Returns

A special situation applies if you have a callable CD, which allows the issuer to end the CD term early. They would typically choose to do this if interest rates decline, and they can issue new CDs at lower rates than they are paying you.

When a CD is called, you are left with the option to choose another investment for your cash or invest in a new CD at the current rate. Either option would generally lead to a significant reduction in interest income when rates are declining.

Some Investments Provide Growth Opportunities When Rates Decline

A period of declining interest rates typically reduces cash yields, but other investments can profit from lower rates. Some of the most common investment choices during a period like this are bonds, stocks, and real estate.

Bond Prices Typically Rise as Interest Rates Fall

Bonds are a type of debt issued by governments and businesses to borrow money from investors for a specific period of time, generally at a set interest rate. Buying bonds when interest rates are high allows you to draw steady income for the life of the investment and provides the option to sell the bond for a profit when interest rates fall.

For example, if you bought a 10-year bond at a rate of 4% and yields for similar newly issued bonds fell to 3%, you would continue to collect interest at the 4% rate. You would also have the option to sell the bond for a profit, since the price of a bond moves counter to its yield.

Stocks and Real Estate Can Outperform During Periods of Low Rates

Like bonds, stocks can also provide superior returns compared to cash investments when interest rates fall. Lower interest rates mean companies may pay less for variable rate loans, directly reducing expenses. Further, businesses are more likely to pursue expansionary activities when financing is inexpensive, leading to potentially higher revenue. Both lower expenses and higher revenue support the company’s profitability and stock price.

Real estate is another avenue to grow your investments as interest rates decline. Lower interest rates generally make real estate more attainable, leading to more sales and more competition between buyers. Ultimately, these trends have historically provided higher profits for sellers and investors.

Between bonds, stocks, real estate, and other investments, there are many avenues to strengthen your portfolio during a period of declining interest rates. You can even take a sector-specific approach and seek to invest in industries or businesses that typically benefit from lower borrowing costs.

Tailor Your Portfolio to Make the Most of Low Rates

When adjusting your portfolio during a period of declining rates, real estate and sector-specific stock investments may be appropriate if you are growth-oriented and don’t need your funds immediately. On the other hand, bonds and dividend-paying stocks may be better options if you are relying on steady income from your investments. Further, you may find that a cash equivalent investment is the most comfortable position for you regardless of real returns.

The important decision of where to invest your money requires a holistic view of your entire financial plan, the historical ramifications of declining rate cycles, and broad economic expectations. Fortunately, you don’t have to tackle this comprehensive review alone. An experienced financial advisor can help.

Discuss Your Investment Plan with Meld Financial

At Meld Financial, we understand the desire to protect your hard-earned money in ultra-safe cash investments. Our experienced advisors can help you balance this desire with the need to grow your funds faster than the inflation rate, and tailor your portfolio to changing economic conditions.

Over four decades of helping clients achieve their financial goals, we have developed a comprehensive wealth management program called Financial Fingerprint®. This nimble plan changes with the economy and your personal circumstances to keep you poised for financial success.

To learn more about Financial Fingerprint® and get started today, contact a member of our team.